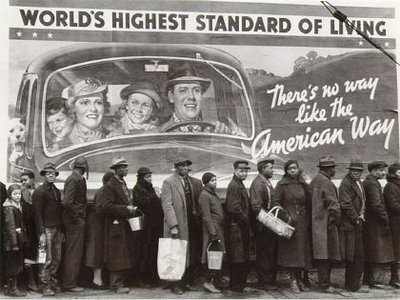

Recently, the economics editor of the Guardian newspaper in the UK, Larry Elliott, presented us with a comparison of the Great Depression of the 1930s and now. In effect, Elliott argued that the world economy was now in a similar depression as then. The 1930s depression started with a stock market crash in 1929, followed by a global banking crash and then a huge slump in output, employment and investment. In that order. The number of bank failures rose from an annual average of about 600 during the 1920s, to 1,350 in 1930 and then peaked in 1933 when 4,000 banks were suspended. Over the entire period 1930-33, one-third of all US banks failed. But it was the stock market crash that was first.

The Long Depression, as I like to call the current one, started with a housing crash in the US, only then followed by a banking crash that was global and then a huge slump in output, investment and employment. The aftermath in both depressions was a long, slow and weak economic recovery with many national economies still not returning to pre-crash levels of output, investment or profitability.

By the way, if anybody doubts that the major economies (G20) are not in what I call a Long Depression, defined as below-trend growth in output, investment, productivity and employment, then consider this nice summary by Wells Fargo bank economists of the key indicators since the end of the Great Recession in 2009 for the US, the economy that has recovered the most.

They conclude that during the 2008-2015 period, the average annual reduction in the level of real GDP from trend was 9.9 percent, 9.8 percent in personal consumption and 10.7 percent in real disposable personal income. During the same time period, the average annual loss in business fixed investment was 20.1 percent, 7.8 percent in employment and 6.9 percent in total factor productivity. The average reduction in the labor force was 2.2 percent, 7.9 percent in labor productivity and 6.4 percent in capital services during the 2008-2015 period.

“And there has been long lasting damages from the Great Recession as the level (trend) of potential series (for all variables) has shifted downward. These results are consistent with the overall economic environment since the Great Recession. That is, a painfully slow economic recovery along with a slower growth in the personal income, employment, wages and business fixed investment.”

Elliott points out that very few economists or pundits predicted the crash of 1929 at the height of huge credit-fuelled boom in stock markets and economic expansion. Similarly, very few forecast the US housing crash and subsequent global financial meltdown. But some did.

The more interesting part of Elliott’s account are the reasons given for the Great Depression of the 1930s and whether they are the same reasons for the current Long Depression. Elliott quotes the biographer of Keynes, Lord Skidelsky, that the main cause was excessive debt. “We got into the Great Depression for the same reason as in 2008: there was a great pile of debt, there was gambling on margin on the stock market, there was over-inflation of assets, and interest rates were too high to support a full employment level of investment.”

This explanation is almost the conventional one among leftist and heterodox economists. Skidelsky combines the views of post-Keynesians (Steve Keen, Ann Pettifor) and some mainstream economists (Mian and Sufi) who highlight the levels of private sector debt (particularly household debt) – “great pile of debt” – with the view of Keynes that “interest rates were too high to support full employment”.

Indeed, next month, Steve Keen, leading post-Keynesian and Minskyite, publishes a new book in which he argues that “ever-rising levels of private debt make another financial crisis almost inevitable unless politicians tackle the real dynamics causing financial instability.” Ironically, And Anne Pettifor has just published a new book that seeks to argue that printing money (more debt?) could help take the capitalist economy out of its depression.

Now there is a lot of truth in the argument that excessive debt (or credit, which is just the other side of the balance sheet) is a prime indicator of impending financial crashes. Debt was high in the 1920s before the crash. This has been documented by many studies, including the seminal work of Rogoff and Reinhart. And Claudio Borio at the Bank of International Settlements has also built up a weight of evidence to show that it is the level and rate of increase or decrease in credit (in effect, a cycle of debt) that is much better indicator of likely financial crashes than the neo-Keynesian idea of some secular stagnation in growth and a collapse in ‘aggregate demand’ (a la Paul Krugman or Larry Summers).

And it is no accident that Steve Keen was one of the few economists to predict the impending crash of 2008. In my book, The Long Depression, I devote a whole chapter to this issue of debt – what Marx called fictitious capital. Credit allows capital accumulation to be extended beyond the creation of real value, for a time. But it also means that when the eventual contraction in investment comes because profitability in productive sectors falls, then the crash is that much greater as debt must be written off with the devaluation of capital values. Credit acts like a yo-yo, going out and then snapping back. So ‘excessive debt’ is undoubtedly a ‘cause’ of crashes, in that sense. The question is what makes it ‘excessive’ – excessive to what? Borio says excessive to GDP growth, but then what determines that?

The other argument that is linked to the ‘excessive debt’ cause is rising inequality as the cause of the crashes of the 1929 and 2008. As Elliott puts it: “while employees saw their slice of the economic cake get smaller, for the rich and powerful, the Roaring Twenties were the best of times. In the US, the halving of the top rate of income tax to 32% meant more money for speculation in the stock and property markets. Share prices rose six-fold on Wall Street in the decade leading up to the Wall Street Crash. Inequality was high and rising, and demand only maintained through a credit bubble.” Yes, similar to the period up to 2008.

Now I don’t think that rising inequality was the cause of the crisis of the 1930s or in 2008 and I have detailed my arguments against the view in several places. The empirical evidence does not support a causal connection from inequality to crash. Indeed, a new study byJW Mason presented at Assa 2017 in Chicago adds further weight to the argument that rising inequality and the consequent (?) rise in household debt was not the cause of the financial crash of 1929 or 2008. “The idea is that rising debt is the result of rising inequality as lower-income households borrowed to maintain rising consumption standards in the face of stagnant incomes; this debt-financed consumption was critical to supporting aggregate demand in the period before 2008. This story is often associated with Ragnuram Rajan and Mian and Sufi but is also widely embraced on the left; it’s become almost conventional wisdom among Post Keynesian and Marxist economists. In my paper, I suggest some reasons for skepticism.”

The gist of my view is that inequality is always part of capitalism (and for that matter class societies, by definition) and rising inequality from the 1980s in the neo-liberal period went on for decades before there was the crash. It is more convincing that rising profitability and a rising share going to capital from labour in accumulation was the cause of rising inequality, not vice versa. So the underlying cause of the eventual slump must be found in the capitalist accumulation process itself and some change in the profit-making machine.

The third cause or reason offered by Elliott for the Great Depression of the 1930s and the Long Depression now is that there is no hegemonic power in a position to act as a ‘lender of last resort’ to bail out banks and national economies with credit and also set the rules for global economic recovery. Between the two world wars, the UK was no longer hegemonic as it had been in mid-19th century and the US was unable or unwilling to take its place. So there was, in effect, no global banker and thus anarchy and protectionism in the world economy.

This was the main argument of the great economic historian, Charles Kindleberger, with his “hegemonic stability theory” in his book, The World in Depression, 1929-39. This theory of international crises has been followed on by such economic historians as Barry Eichengreen and HSBC economist, Stephen King, cited by Elliott as saying, “There are similarities between now and the 1930s, in the sense that you have a declining superpower”. So the argument goes that the US is now no longer hegemonic and cannot impose international rules of commerce as it did after 1945 with the IMF, the World Bank and GATT. Now, there are rival economic powers like China and even the European Union that no longer bend to US will. And the IMF is no position to act as lender of last resort to bail out economies like Greece etc.

This view also comes from Marxist economists like Leo Panitch and Sam Gindin, who (conversely) argue that the US is still a hegemonic power and thus still decides all in an “informal American empire” and this explains the huge economic recovery after the 1980s in the neo-liberal period. Yanis Varoufakis argues something similar in his book, The Global Minotaur. Skidelsky too likes the argument that the neoliberal ‘recovery’ was achieved by globalisation under US imperial control. “Globalisation enables capital to escape national and union control.” He considers this the Marxist explanation: “I am much more sympathetic since the start of the crisis to the Marxist way of analysing things.”

But is the crisis of the 2008 the result of weak US imperial power or too much US power? Either way, I doubt that the hegemonic stability theory is a sufficient explanation of the Great Depression or the Long Depression. Clearly, the US has been in (relative) decline as the leading imperialist power economically, although it remains the leading financial power and overwhelmingly dominant as a military power – similar to the Roman empire in its declining period.

No doubt that this has had some effect on the ability of all the major capitalist economies to get out of this depression and increased the move towards nationalism, protectionism and isolationism that we now see in many countries and in Trump’s America itself now. But the end of ‘globalisation’ was not the result of weakening American power but the result of the slowdown in global investment, trade and, above all, in the profitability of capital that empirical evidence has revealed since the late 1990s. The ‘death’ of globalisation was accelerated by the global financial crash and the collapse in world trade and debt flows since 2008.

The long depression has continued not because of high inequality or the weakening of US hegemony or because of the move to protectionism (that has hardly started). It has continued, I contend, because of the failure of profitability to rise sufficiently to revive productive investment and productivity growth; and the continued hangover of fictitious capital and debt. Indeed, I have shown thatthese are the same reasons that extended the Great Depression of the 1930s: low profitability, high debt levels and weak trade.

In Elliott’s article we are also offered some differences between the 1930s and now. The first is that, unlike the 1930s, now central banks acted to boost money supply and bail out the banks with interest-rate cuts to zero and quantitative easing. Back in the 1930s, according to Adam Tooze in his book The Deluge, deflationary policies were pursued everywhere. “The question that critics have asked ever since is why the world was so eager to commit to this collective austerity. If Keynesian and monetarist economists can agree on one thing, it is the disastrous consequences of this deflationary consensus.”(Tooze).

And they did agree on this in the current depression. As I have shown in several posts, former US Fed chief Ben Bernanke was a mainstream expert on the causes of the Great Depression and once told a meeting of the mainstream to commemorate his mentor, the great monetarist, Milton Friedman, that the mistake of the 1930s not to expand the money supply would not be repeated. But QE and easy money may have bailed out the banks and restored ‘business as usual’ fro them, but it did not end the current Long Depression. Actually, that easy money and unconventional monetary policy would end the Great Depression was thought possible by Keynes in 1931. But by 1936, when he wrote his famous General Theory, he realised it was inadequate. And indeed, the idea that things would be different this time compared to the 1930s because of easy monetary policy has turned out to be bogus.

The Keynesians, having in many cases advocated easy money as the way out of the current depression, now push fiscal stimulus as the solution, just as Keynes finally resorted to in 1936. Keynesians like Skidelsky claim that the UK had fiscal ‘automatic stabilisers’ that were kicking in to ameliorate the slump of the 1930s but the governments of the day smashed those and imposed austerity and that caused the extension of the slump into depression.

Most governments now have not adopted massive government spending or run large budget deficits to boost investment and growth – mainly because they fear a massive increase in public debt and the burden that will put on funding it from the capitalist sector. So we hear from the battery of leftist and Keynesian economists that the application of ‘austerity’ is the cause of the continued Long Depression now. It is difficult to prove one way or another, but in a series of posts and papers, I have put considerable doubt on the Keynesian explanation of the Long Depression.

The New Deal did not end the Great Depression. Indeed, the Roosevelt regime ran consistent budget deficits of around 5% of GDP from 1931 onwards, spending twice as much as tax revenue. And the government took on lots more workers on programmes – but all to little effect.

Coming off the gold standard and devaluing currencies did not stop the Great Depression. Indeed, resorting to competitive devaluations and protectionist tariffs and restrictions on international trade probably made things worse.

And monetary easing has not worked this time and nor has fiscal stimulus (as Abenomics in Japan has shown), which we shall see again if Trump ever does manage to run budgets deficits to lower corporate taxes and increase infrastructure spending.

Now it seems protectionism and devaluations are becoming more likely in this post-Trump, post-Brexit period of the Long Depression. Indeed, the latest policy document for the upcoming G20 summit in Germany next week has actually dropped its condemnation of protectionist policies. As Elliott sums it up: “So far, financial markets have taken a positive view of Trump. They have concentrated on the growth potential of his plans for tax cuts and higher infrastructure spending, rather than his threat to build a wall along the Rio Grande and to slap tariffs on Mexican and Chinese imports. There is, though, a darker vision of the future, where every country tries to do what Trump is doing. In this scenario, a shrinking global economy leads to shrinking global trade, and deflation means personal debts become more onerous.”

The Great Depression only ended when the US prepared to enter the world war in 1941. Then government took over from the private sector in directing investment and employment and using the savings and consumption of the people for the war effort. Profitability of capital rocketed and continued after the end of the war. Looking back, the depression of the 1880s and 1890s in the major economies only ended after a series of slumps finally managed to raise the profitability of capital in the most efficient sectors and national economies and so delivered more sustained investment – although eventually that led to imperialist rivalry over the exploitation of the globe and the first world war.

How will this Long Depression end?

Originally posted at The Next Recession.

Leave a Reply